Social Security Benefits by Age 2026: When to claim Social Security retirement benefits is considered to be one of the most crucial decisions people in America face before their retirement period. In 2026, millions of retirees will continue comparing the advantages of claiming benefits early at age 62, waiting until FRA, or delaying until age 70 for larger monthly checks.

According to the current Social Security Administration rules, those who choose to receive their benefits after age 70 may receive the highest benefit amount monthly. increase happens because the Social Security system applies delayed retirement credits for every month benefits are postponed after FRA.

According to the SSA, the truth remains that retirement benefits keep increasing until 70 and do not increase further. Those who choose to file later are entitled to higher payments, though the right filing age varies depending on personal finances and health.

Social Security Benefits by Age 2026

Social Security benefits change dramatically based on when one opts to take them. Social Security benefits in the year 2026 may see the highest payment for beneficiaries aged 70. The benefits paid at this point are much higher compared to individuals receiving their benefits at age 62.

This happens due to delayed retirement credits that increase one’s Social Security benefits by 8% for each year one postpones retirement beyond the full retirement age, up until 70 years. Social Security payments may begin as soon as one reaches 62 years of age; however, a reduction is applied for taking the payments early.

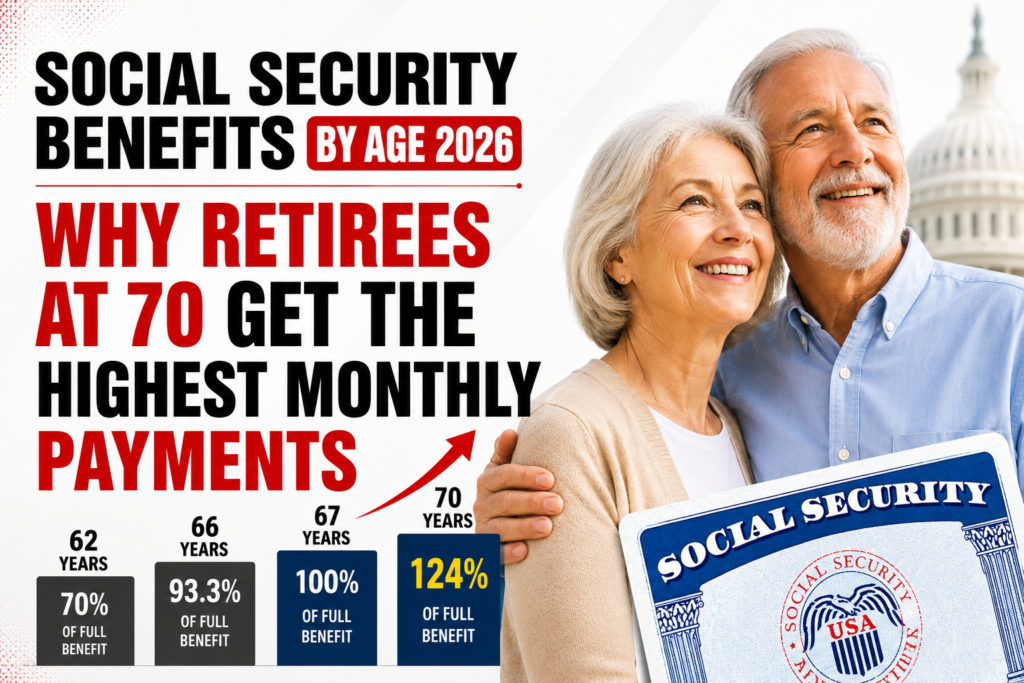

One gets his or her full benefit only at one’s full retirement age, which varies from 66 to 67 years depending on birth year. At age 70, one gets an even higher benefit that is 24% to 32% more.

Why Retirees at 70 Get the Highest Monthly Payments

Individuals who retire at the age of 70 receive the highest monthly benefits because they accumulate delayed retirement credits for each year they postpone taking Social Security beyond their full retirement age. If they do so, their Social Security benefit increases by 8% for each year they delay their claiming and this increase applies to the rest of their lives.

For example, if an individual was born after 1960 (full retirement age is 67) and his/her calculated benefit at the time of his/her full retirement age is $2,000 per month, then taking the Social Security at the age of 62 results in receiving only $1,400 per month (30% less), but delaying it until the age of 70 leads to receiving $2,480 per month (24% more).

Thus, $1,080 more per month (or $12,960 more per year) is received by postponing for 3 years. After the age of 70, the 8% raise does not apply, meaning that the additional waiting period does not provide any extra benefit. At age 70, one receives the maximum benefit of $5,181 in 2026, while at the age of 62, it is $2,969 and $4,152 at FRA.

Social Security Claiming Age Comparison (2026)

Example: Assume Isabella qualifies for a Social Security benefit of $2,000 per month at her FRA (67).

| Claiming Age | Monthly Benefit | Annual Benefit | Difference from FRA | Simple Example |

|---|---|---|---|---|

| 62 | $1,400 | $16,800 | 30% lower | Isabella starts receiving money immediately but accepts a permanently reduced monthly payment. |

| 67 (FRA) | $2,000 | $24,000 | Full benefit | Isabella receives her complete earned retirement benefit with no reduction. |

| 70 | $2,480 | $29,760 | 24% higher | Isabella waits longer and receives the highest monthly benefit available. |

Real-Life Comparison Example

3 Friends, Same Earnings Record

Assume Charlotte, Emma, and Evelyn all qualify for a $2,000 FRA benefit at age 67.

| Name | Claiming Age | Monthly Benefit | Annual Benefit | Main Reason |

|---|---|---|---|---|

| Charlotte | 62 | $1,400 | $16,800 | Wants income immediately after leaving work. |

| Emma | 67 (FRA) | $2,000 | $24,000 | Retires at Full Retirement Age and takes the full benefit. |

| Evelyn | 70 | $2,480 | $29,760 | Uses savings first and waits for the largest possible check. |

Difference in Monthly Payments

| Comparison | Extra Monthly Amount |

|---|---|

| Evelyn (70) vs Charlotte (62) | $1,080 more |

| Emma (67) vs Charlotte(62) | $600 more |

| Evelyn (70) vs Emma(67) | $480 more |

Break-Even Example Table

| Scenario | Claim at 62 | Claim at 70 |

|---|---|---|

| Monthly Benefit | $1,400 | $2,480 |

| Benefits Received Before Age 70 | $134,400 | $0 |

| Extra Monthly Benefit After 70 | – | $1,080 more |

| Approximate Break-Even Age | – | Around 80–81 |

Why Many Americans Rush to Claim Early

Despite the fact that waiting until 70 allows getting maximum monthly checks, most Americans prefer to claim early. The typical claiming age is 64. The reasons include the following:

- Fear of Running out of Money: About one-half of the people choose to claim early as they are afraid Social Security will go bankrupt. In fact, there are no risks of complete insolvency. Even if the trust fund dries up in about 2034, Social Security may continue paying benefits at as per the amount decided by it.

- Poor Health and Low Life Expectancy: Those Americans who have been ill for many years or have low life expectancy claim early saying, “Better I take benefits now than die before having them.”

- Loss of Work: A lot of people retire before reaching 62, losing job, or unable to work any longer. They just have to start collecting benefits to cover daily expenses.

- They Think They Have Earned It: Some Americans say, “I paid Social Security for 35 years, so this is my money and I should receive it now.”

- Worry about Passing Away Before Collecting: Individuals are afraid that they will pass away before age 65 or 66 and receive nothing. They would rather collect less money now than wait for nothing.

- Excessive Fear About Finances: Market failures, job security, and high costs contribute to fear about finances, and individuals would prefer to receive money now than worry later.

Is Waiting Until 70 the Best Choice?–who should claim when

However, for many healthy individuals with other sources of income, waiting until they turn 70 is the best possible solution since they will receive the highest monthly payments throughout their lifetime this figure might reach up to 24% higher when compared with filing claims at FRA and even 75% more than those claiming at 62.

Example for this situation: Richard, age 67, has $500,000 in savings and a pension. He is in good health (his parents lived to 90). Waiting until 70 gives him $1,080 more per month for life and that’s the best financial move.

If you are in poor health, or your parents died young, or if you need the money right away to meet expenses since you either lost your job or cannot work, then it makes sense to claim sooner rather than later.

Example for this situation: Sarah, age 62, has diabetes and heart disease. Her father died at 68. She has some savings but no pension. Claiming at 62 is the right choice because she may not live to 78 anyway.

Wrap-Up

The age at which Americans collect Social Security benefits remains important when considering the calculation of monthly retirement income as of 2026. Although an individual is eligible to start collecting their benefits starting at age 62, choosing this option usually means that the amount collected will be smaller due to the reduction.

Individuals who claim their benefits at the Full Retirement Age receive the maximum monthly income since they receive their total amount. However, waiting until age 70 can mean receiving the most significant monthly income due to deferred retirement credits.

While delaying Social Security benefits may result in better income, there is no one-size-fits-all approach to determining the best claiming age. Personal considerations and an understanding of how Social Security benefits work may help individuals make a more informed decision about their future income.

Disclaimer: This article provides general information based on official SSA data as of 2026. Individual benefits depend on your earnings history and circumstances. Always verify your benefits through your official SSA account at ssa.gov. Social Security rules may change over time, so keep checking the official website.

Frequently Asked Questions

At what age can one start receiving Social Security retirement payments?

One can start receiving Social Security payments from the age of 62, but there will be reductions in monthly payments

What is meant by the Full Retirement Age?

The full retirement age for most current retirees is 67, when they get their full earned amount of retirement benefit.

Will my Social Security benefits increase if I wait longer than the FRA?

Yes. Benefits usually increase by about 8% per year for each year you delay claiming after FRA, up to age 70.

Can I work while collecting Social Security benefits?

Yes, one can work even while collecting Social Security benefits. But if you are below FRA and earns more than SSA, their monthly benefit amount might be reduced.

Ritika's writing philosophy is built on one core principle: every person deserves access to clear, accurate, and actionable benefit information — without having to wade through confusing government language. Her guides are trusted by seniors, working families, and low-income households across North America who rely on timely payment updates and eligibility information.

All content written by Ritika is thoroughly research-based, sourced from official government portals including SSA.gov, Canada.ca, and CRA publications.